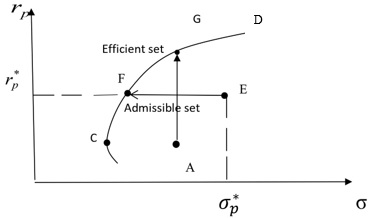

In this study attention is focused on the possibility of applying the theory of effective and admissible sets by H. Markowitz [1, p. 85-90] for the diversification of the portfolio of risky investments. According to the algorithm for constructing the admissible set, the portfolio that is more effective in terms of expected profitability and riskiness for the investor will be located higher and to the left on the "expected profitability - riskiness" plane. Portfolios that are elements of the effective set will be optimal. Such portfolios are Pareto-optimal.

We consider the problem of optimal portfolio diversification under constraints. Let's move on to the second problem in the general formulation of H. Markowitz about optimizing the risk of the portfolio of shares that is optimal in terms of expected profitability [2]. For this, we will use sets of admissible and efficient portfolios corresponding to the selected set of shares.

Figure 1: Admissible and efficient sets of portfolios of risky securities

The risk optimization procedure for the optimal expected return portfolio consists in choosing at each step admissible portfolios that lie on the EF line. This line connects point E, that corresponds to the optimal market value of the portfolio, and point F, that belongs to the efficient set. The peculiarity of this selection of the optimal portfolio is that on this straight line, according to the definition, each of the portfolios corresponds to the same expected return, but the riskiness decreases in the direction of the axis. This property of the admissible set of investment portfolios allows, on the one hand take into account the restrictions

and on the other hand - to determine the portfolio of "optimal" expected return with less risk. Another mathematical formulation of the problem of optimization of the expected profitability rp (T) of the investment portfolio at a certain time T level of its risk τ is as follows [3, p. 52-54]

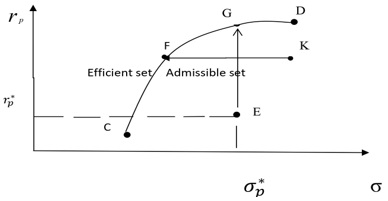

The procedure for optimizing the portfolio's expected return rp for a certain level of risk consists in choosing at each step admissible portfolios.

Figure 2: Optimizing the market value of the stock portfolio

That lie on the line EG connecting point E, which corresponds to the optimal portfolio calculated by expected return, and point G, which belongs to the efficient set. This line is parallel to the axis of market value rp. The peculiarity of this selection of the optimal portfolio is that on this straight line, according to the definition, each of the portfolios corresponds to the same riskiness, but the market value rpincreases. If the defined portfolio is located at point K, that is, one for which there is no possibility to increase the expected return, according to the rule proposed above, then the "optimal portfolio" is determined by moving it from K to F, which is an element of the effective set of portfolios. In fact, this means reducing the riskiness of the stock portfolio. The effective set or the set of effective portfolios in figures 1,2 is on the arc.

Prospects for research in this applied field can also be linked to the combination of technical and fundamental analysis methods together with artificial intelligence approaches. Such attempts have been made in the work [3], as well as in the studies of other authors. This study is one of the attempts to effectively combine these approaches to decision-making when investing in securities.

Conclusion. In this study new mathematical formulations of the optimization problems of the stock portfolio structure are given and methods of their solution are developed. Mathematical problems formulated on the basis of models of the dynamics of the market value of one share and a portfolio of shares [3] make it possible to solve the problem of optimal diversification of the investment portfolio, taking into account quantitative and qualitative market restrictions on the portfolio structure.

References:

1. Markowitz H. Portfolio selection, Journal of Finance. 1952, pp. 77-91. https://doi.org/10.1111/j.1540-6261.1952.tb01525.x.

2. Sharpe W., Alexander G., Bailey J., Prentice Hall, 1999 – Business & Economics – 962 pages.

urn:lcp:investments0000shar: epub:d11a8121-e60c-477b-8c35-faa99a933f6c.

3. Kulian, V., Yunkova, O., Korobova, M. Solutions sensitivity when modeling of investment dynamics. Bulletin of Taras Shevchenko National University of Kyiv. 2022, no. 4, pp. 51-54. https://doi.org/10.17721/1812- 5409.2022/4.6.

|