There is a growing body of literature that recognises the importance of the market price of risk estimation. It is sometimes referred to as the ‘most important number’ in the financial industry, because it determines the realised returns associated with risky investments. In a more precise economic sense it can be interpreted as the rate of return above the risk-free rate, per unit of risk, where risk is usually characterised by the asset volatility (see, e.g., Hughston & Hunter 1999). It follows that the market price of risk can play a significant role in addressing the issue on how investors should make investment decisions in financial markets. One of the main obstacles in determining the market price of risk is to reach a consensus on how it should be computed. Indeed, it is a great theoretical as well as practical issue that has dominated financial economics for many years. Although extensive research has been carried out on how to estimate the market price of risk, there is no unique technique to determine it. For instance, in the report by J. P. Morgan (2008), four different approaches to the market price of risk estimation are represented, in particular, estimations based on (i) dividend discount model, (ii) historical average of realised returns, (iii) yield method, and (iv) bond-market implied risk premium. The estimated mean values fall within a range of 3% ∼ 13% whereas, but in fact, it might fluctuate within a much wide range of −200% ∼ +200%.

In a recent publication by Brody & Hughston (2013), a new method for the estimation of the realised market price of risk has been proposed within the context of a single-asset single-factor setup. A key aspect of the this new approach is the introduction of an ‘information process’ that models the market flow of information concerning the hidden value of the market price of risk. It has been shown, in particular, that provided that the knowledge concerning the probability distribution of the hidden market price of risk is available, then the realised value of the asset return becomes measurable with respect to the information associated with the price dynamics. A drawback of this method, however, is that it is only applicable to a market consisting of only a single risky asset; whereas for a practical application of the theory, with the view towards its implementation, a multi-asset extension is crucial. With this in mind, the present thesis represents the theory to accommodate multi-factor multi-asset setup. The key to our approach is to rotate the volatility vectors for the given set of correlated risky assets to generate a family of independent portfolios. The method of Brody & Hughston (2013) can then be applied individually to these portfolios, because they are independent. Having obtained the market prices of risk for these portfolios, those for the original assets can be recovered by means of a reverse rotation.

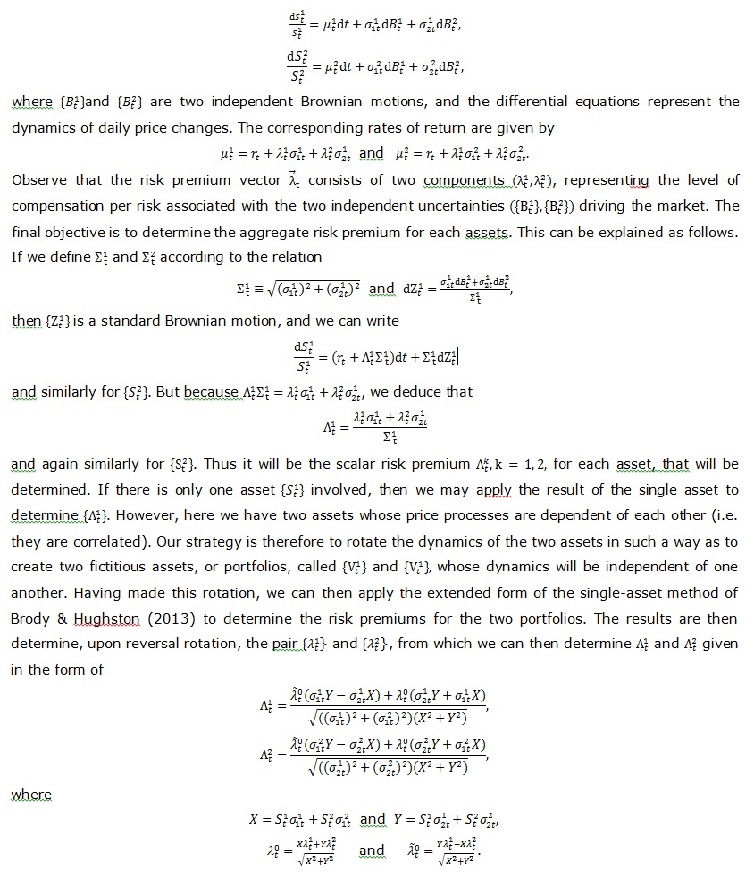

For the purpose of estimation of the market price of risk for different market sectors, let us begin by considering a two-factor, two-asset model, which will be sufficient to illustrate the approach that we will be proposing in this thesis. Since the number of assets agrees with the number of factors, market completeness is assumed in this setup. We let the price processes of the two assets be given respectively by {S1t} and {S2t}, both driven by two-factor Brownian motions. The dynamics of these price processes are given by

References:

1. D. C. Brody & L. P. Hughston (2013) L ́evy information and the aggregation of risk aversion . In: Proc. Roy. Soc. Lond. 469.

2. E. Elton, M. Gruber, S. Brown & W. Goetzmann (2014) Modern Portfolio Theory and Investment Analysis. Ninth Edition (New Jersey: Wiley).

3. L. P. Hughston & C. J. Hunter (1999) Financial Mathematics: An introduction to derivative pricing.

4. J. C. Hull (2015) Options, Futures, and Other Derivatives (Boston: Pearson Education, Inc.).

5. R. Litterman & K. Winkelmann (1998) Estimating Covariance Matrices. In: Risk Management Series (R. A. Krieger, eds), New York: Goldman Sachs & Co.

6. D. Ruppert (2004) Statistics and Finance: an Introduction.

|